Local business tax

Taking account of the transfer pricing adjustment

According to the amendment, the local business tax base may also be reduced by the amount of the transfer pricing adjustment if the related party does not disclose the numerical effect of the symmetrical adjustment in its local business tax return because the transaction concerned is not relevant for the determination of the tax base (e.g. it is recognised as a cost of services used). In such case, the related party's statement should state that it has taken the adjustment into account in determining the foreign tax base equivalent to the local business tax or, failing that, the corporate income tax or foreign tax base equivalent to the corporate income tax.

Simplified tax base assessment

The amendment updates the current, partly overlapping and difficult-to-understand three options for simplified tax base assessment, which will be replaced from 2023 by the following single method ("itemised assessment method"):

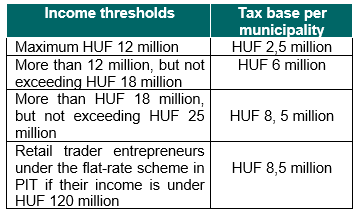

Eligible persons:

- All entrepreneurs whose annualised income for the tax year does not exceed HUF 25 million (HUF 120 million for retail trader entrepreneurs under the flat-rate scheme in personal income tax).

Income includes:

- for sole entrepreneurs subject to the Personal Income Tax Act: their income under the PIT Act;

- for taxpayers in the scope of the Act on the Fixed-Rate Tax of Low Tax-Bracket Enterprises (“KATA Act”): income under the KATA Act;

- other entrepreneurs, companies: net turnover under the Local Business Tax Act.

Opting for the itemised assessment method:

The itemized assessment method may be elected only for the entire tax year. The entrepreneur's election remains valid until withdrawal, but the entrepreneur is bound by his choice in respect of both his headquarters and each permanent establishment (the taxpayer should duly notify the municipality, where he sets up a new business establishment / moves his headquarters to, when a new establishment is set up or the headquarters moved to during the year).

The election should be notified by the last day of the 5th month of the tax year for which the method should be applied. Start-up companies may decide to opt for this method by the last day of the deadline for their tax return for the first tax year.

Opting out of the itemised assessment method:

If the entrepreneur no longer wishes to apply the itemised assessment method, he may opt out by the last day of the 5th month of the tax year concerned (simultaneously with the notification, he should also declare a local business tax advance under the general rules).

If the entrepreneur is no longer allowed to apply the itemised assessment method because he exceeded the income threshold in the current tax year, the method should not be applied either for the current year, or the following tax year.

Assessment of the itemised tax base:

If the tax year is shorter than 12 months, the entrepreneur should take into account the pro rata temporis reduction of the taxable base when determining the taxable base for the tax year.

The key points of simplification:

- The local business tax base should not be determined for, tax returns should not be filed for and the tax base should not be apportioned between the municipalities of the establishments;

- There is an obligation to pay the advance tax once a year and, if the annual income is below the upper limit of the relevant income bracket, no further tax liability or tax return obligation should arise;

- An obligation to file tax returns should only arise if the entrepreneur's income for the previous tax year increases resulting in the change of the relevant income band. In such case, the tax differential should also become payable;

- If the entrepreneur's taxable amount in the current year is below the lower limit of the income band to which he was subject to previously, a tax refund arises which can be claimed back by filing a tax return;

- Under the itemised assessment method, the entrepreneur should not be entitled to any tax exemptions, tax relief or tax reductions under the law or municipal regulations. Therefore, in the case of entitlement to a higher amount of tax relief, it is recommended to assess the tax base under the general method.

Transitional rule for new KATA-taxpayers

KATA-taxpayers who would have to file a local business tax return by 15 January 2023 because they wish to claim a tax credit or reduction, may do so by 31 May 2023 instead of 15 January 2023. So KATA-taxpayers also have 5 months to decide whether to apply of the new itemised assessment method for the tax year 2023 (coming into effect from 1 January 2023). The legislation gives them a presumption that they should wish to apply the new method, therefore, if they do not wish to apply it, they should notify their decision towards the tax authority in their 2022 tax returns.

Deduction of CoGs and re-charged services from the taxable base in special cases

Taxpayers engaged in certain activities (typically the sale of separately regulated goods) are not subject to the requirement that Cost of Goods Sold (“CoGs”) and the cost of re-charged services may be deducted only on a pro rata basis. These taxpayers have previously also applied special provisions which allowed them to deduct the full amount of the CoGs and re-charged services from the tax base.

These special rules have been amended with effect from 1 January 2023.

While the special rules for taxpayers performing export sales, as well as taxpayers who have domestic sales of publicly financed medicines (as goods) have not changed, the rules for other categories of taxable persons have been amended as follows:

-

- a new category of taxpayers has become entitled to a full deduction: those supplying transport services as national transport organisers;

- for taxpayers providing clearing house services for energy products, a minor clarification of the special rule has been introduced, which removes the hitherto over-regulated definition of goods, materials and services used for the settlement of transactions in the natural gas and electricity markets;

- a similar clarification as above has been made for the taxpayers involved in the supply of tobacco products subject to government authorisation.

Simplified tax base assessment for companies taxed under the Small Business Tax Scheme (the „KIVA”)

Companies taxed under the KIVA scheme are still entitled to assess their local business tax base at 20% of their Small Business Tax base. Minor clarifications have been made to the detailed rules.

Transition to IFRS reporting

The amendment specifies that if a company is merged into another company simultaneously with transiting to the IFRS reporting, the successor company should be entitled to claim / obliged to pay the transition difference.

***

Should you have any questions regarding this newsletter,

the tax experts of VGD Hungary will be pleased to assist you.

This newsletter provides general information and does not constitute tax advice